Aviva plc Q1 2026 Trading Update

May 14, 2026 – (London, UK) – To read this update in full, please click here.

Benefits of diversified model evident with strong growth in capital-light businesses

Combined operating ratio improving and on course for 2026 guidance

Firmly on track to meet Group targets

Amanda Blanc, Group Chief Executive Officer, said:

“We have delivered another quarter of strong trading, building momentum in 2026. We delivered profitable growth across Aviva despite global market volatility, demonstrating yet again the advantages of our market-leading positions and diverse business model.

“We made excellent progress in General Insurance, growing premiums by 19% and improving profitability significantly in the UK, Ireland, and Canada. The integration of Direct Line is firmly on track with stronger profitability and policies sold through price comparison websites have nearly doubled since the start of the year. In Wealth, where we are the number one player, we delivered another very positive performance, increasing net flows by 49% to £3.3bn. Our workplace pensions business performed particularly well, increasing net flows by 71%, and the tax-year end was another success, with strong inflows in our adviser platform and direct wealth business.

“We have made an excellent start to 2026. Our continued strong trading performance, high quality balance sheet, and diverse set of leading businesses, gives us confidence that we are well placed to meet our group targets, and deliver even more for our customers and shareholders this year.”

Another quarter of delivery

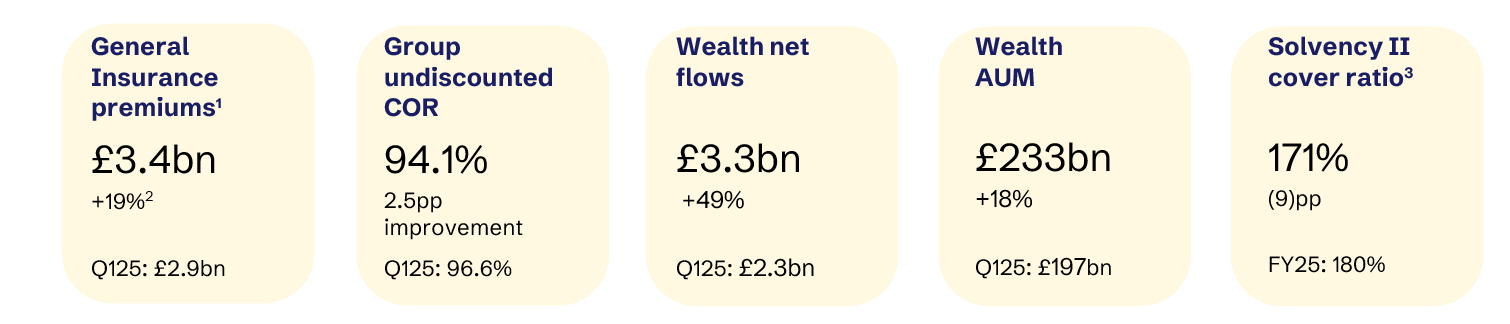

- General Insurance premiums up 19% to £3.4bn (Q125: £2.9bn).

- UK&I GI premiums up 26% to £2.5bn (Q125: £2.0bn) with 59% growth in Personal Lines, supported by both the acquisition of Direct Line and growth in the intermediated channel. Commercial Lines was 7% lower reflecting the impact of the rating environment partly offset by strong retention.

- Canada GI premiums up 3% in constant currency to £0.9bn (Q125: £0.9bn) with Personal Lines up 4% supported by rate actions, and Commercial Lines up 1% reflecting scheme wins in GCS partly offset by the rating environment.

- Group undiscounted combined operating ratio (COR) improved 2.5pp to 94.1% (Q125: 96.6%), with improvements across all markets supported by strong rate adequacy and better weather experience. Discounted COR of 90.0% (Q125: 92.9%).

- Wealth net flows of £3.3bn (Q125: £2.3bn) were up 49% representing 6% of opening Assets Under Management4 (‘AUM’) with strong growth in Platform and Workplace net flows.

- Protection sales of £88m (Q125: £89m) were 2% lower with growth in Group Protection offset by lower Individual Protection which benefited from strong sales in the prior period ahead of changes to stamp duty.

- Health in-force premiums grew 9%, while we maintained a low-90s combined operating ratio. Health sales of £25m (Q125: £37m) were 31% lower reflecting lower market demand in the consumer and SME channels.

- Retirement sales of £1.1bn (Q125: £1.8bn) including Individual Annuities sales up 10% and Equity Release sales up 8%. BPA volumes were £0.6bn (Q125: £1.3bn), as we maintained pricing discipline in a competitive market. BPA year-to-date volumes have now reached £1.1bn with at least low-teen IRRs.

- Aviva Investors net flows of £0.1bn (Q125: £(0.9)bn) saw a strong increase supported by improved external flows. Internal net flows (excluding legacy assets) of £1.1bn (Q125: £1.1bn) reflects £1.5bn of Wealth net inflows and £0.5bn of Direct Line assets transferred, offset by lower annuity new business.

Strong solvency and liquidity positions

- Estimated Solvency II shareholder cover ratio of 171% (FY25: 180%), after deducting 15pp in Q1 for the 2025 final dividend of £800m, previously announced share buyback of £350m and the end of Solvency II grandfathering on £200m of Tier 2 debt. Total capital generation added 6pp over the quarter of which around 2.5pp was from beneficial market movements.

- On track to deliver Direct Line capital synergies of >£350m by the end of the year, which would add >7pp to the shareholder cover ratio, in addition to the c.£150m delivered at year end 2025.

- In line with previous guidance, following achievement of these Direct Line capital synergies, we expect solvency to be above our target range of 160-180% by full year 2026.

- Solvency II debt leverage ratio of 31.6% (FY25: 30.1%) reflecting the Q1 impacts of the 2025 final dividend and share buyback.

- Centre liquidity as at the end of April 2026 of £1.3bn (February 2026: £1.5bn).

Confident outlook

- We are on track to meet our Group targets. Operating EPS of 11% CAGR (2025-28); IFRS Return on Equity of >20% (by 2028); and Cash remittances of >£7bn (2026-28 cumulative).

- In General Insurance, we are carefully managing through the cycle, trading with discipline. For 2026, we are firmly on track to meet our guidance in the UK&I GI business to achieve a COR of <94%, and for the COR in Canada to be approaching 94%.

- We continue to make good progress on the Direct Line integration and remain on track to deliver the cost synergies and capital synergies we previously announced, and are pleased with how the business is performing.

- In Wealth, we expect continued growth momentum underpinned by our Workplace business which continues to see £1bn of inflows from regular member contributions each month. We are on track to meet our ambition for £280m operating profit by 2027.

- In our Health business profitability is strong, though we have observed lower demand in our SME and consumer channels. We are focused on achieving our £100m operating profit ambition in 2026.

- In BPA, while market conditions remain competitive, we are continuing to actively trade and have now written £1.1bn as of today. We will maintain discipline and will only write business that meets our financial hurdles.

Footnotes

1. Sales for Insurance (Protection and Health) refers to Annual Premium Equivalent (APE). Sales for Retirement (Annuities and Equity Release) refers to Present Value of New Business Premiums (PVNBP). Premiums for General insurance refer to gross written premiums (GWP). The first instance of each reference has been footnoted. However, this footnote applies to all such references in this announcement. PVNBP, APE and GWP are Alternative Performance Measures (APMs) and further information can be found in the 'Other Information' section of the Aviva plc Annual Report and Accounts 2025.

2. Q126 includes the results of Direct Line. All GWP movements are quoted in constant currency unless otherwise stated.

3. Solvency II shareholder cover ratio is the estimated Solvency II shareholder cover ratio at 31 March 2026.

4. All net flows as a percentage of opening assets under management are annualised.

5. GWP comparatives for Ireland Personal Lines have been updated for consistent presentation of health premiums.

6. Rounding differences apply.