May 15, 2025 (London, UK) – To read this update in full, click here.

Continued strong momentum with another quarter of growth

Strong and resilient capital and liquidity positions

Confident in achieving Group targets

Amanda Blanc, Group Chief Executive Officer, said:

“Aviva has got off to a great start in 2025. We continue to trade strongly, serving our customers well, growing profitably right across the group, and demonstrating the resilience of our diversified business in a period of market volatility.

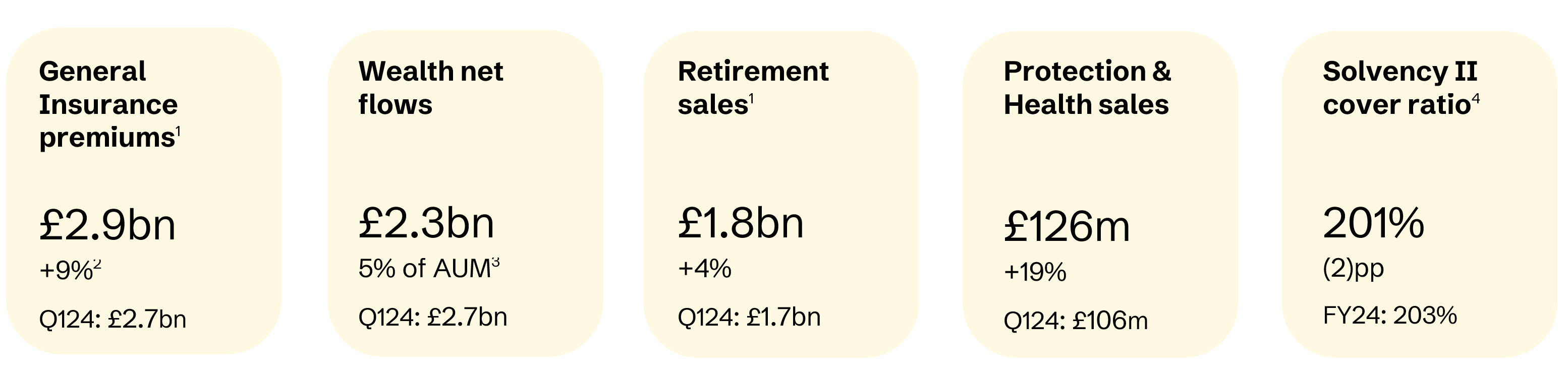

“Aviva has leading positions in growing markets and we have seen excellent trading in a number of areas. General insurance premiums increased by 9%, with strong performances in both personal and commercial insurance, including a travel insurance partnership with Nationwide and the benefits of acquiring Lloyd’s insurer Probitas. In our Wealth business, we secured £2.3 billion of net flows which is an encouraging 5% of opening Assets Under Management, and we increased net flows by 52% in our Platform business. In Retirement, our investment in the business and higher interest rates are driving growth in individual annuities where we increased sales by 32%. We also continue to see high levels of interest in health insurance and we grew sales by 19% with strong demand from consumers and employers.

“The acquisition of Direct Line is firmly on track. Direct Line shareholders voted overwhelmingly in favour of the transaction and we expect to complete the deal in the middle of the year.

“We continue to be very positive about the outlook for 2025. Our balance sheet is strong, we have a clear customer-focused strategy which we continue to deliver at pace and our market-leading businesses are growing well, especially in capital-light areas. We are increasingly confident about Aviva’s prospects and meeting our financial targets.”

Another quarter of high-quality growth momentum

- General Insurance premiums up 9% to £2.9bn (Q124: £2.7bn).

- UK&I GI premiums up 12% to £2.0bn (Q124: £1.8bn) with 8% growth in Personal Lines and 15% growth in Commercial Lines, reflecting strong new business and the acquisition of Probitas.

- Canada GI premiums of £0.9bn (Q124: £0.9bn) up 5% at constant currency (flat in reported currency) with Personal Lines up 10% driven by pricing actions. Commercial Lines was 2% lower as we maintained discipline with focus on margins over volume.

- Group undiscounted combined operating ratio (COR) of 96.6% (Q124: 95.8%). An improvement in the underlying COR as pricing actions taken continue to earn through was more than offset by elevated CAT activity, including Storm Eowyn. Discounted COR of 92.9% (Q124: 92.0%).

- Wealth net flows of £2.3bn (Q124: £2.7bn) represented 5% of opening Assets Under Management (‘AUM’). Strong growth in Platform was more than offset by the outflow of assets of a large Workplace scheme following their decision in 2023 to switch to another provider. As at the end of April, net flows were £4.0bn, representing 6% of opening AUM, and ahead of the prior period (£3.5bn) due to the onboarding of a large Workplace scheme.

- Retirement sales of £1.8bn (Q124: £1.7bn) were up 4% driven by higher volumes in Individual Annuities and Equity Release. BPA volumes of £1.3bn were broadly consistent with Q124. Retirement margin improved to 3.6% (Q124: 2.9%) as we maintain our disciplined focus on margins.

- Protection and Health sales of £126m were up 19% following the completion of the acquisition from AIG in April 2024 and Health in-force premiums were up 11%.

Strong solvency and liquidity positions

- Estimated Solvency II shareholder cover ratio remains strong at 201% (FY24: 203%).

- The movement in the quarter was driven by the final dividend (-8pp), partly offset by total capital generation (+5pp) predominantly reflecting operating capital generated in the quarter and positive market movements. Debt actions were a small positive as the £500m Restricted Tier 1 (RT1) issuance on 31 March is mostly offset by the £450m preference share cancellation5.

- Solvency II debt leverage ratio of 31.9% (FY24: 28.9%), or 30.1% pro forma for the cancellation of the preference shares5.

- Centre liquidity (April 2025) of £1.8bn (Jan 25: £1.7bn). Cash remitted to the Group in order to settle the Direct Line acquisition has been ring-fenced and is excluded from the Group’s Centre liquidity.

Confident outlook

- Our strategy to move Aviva to a more capital-light business continues to deliver. We are already a majority capital-light business with 56% of operating profit6, and the acquisition of Direct Line will take us beyond 70% as synergies and profits are delivered.

- We are confident in meeting the Group targets set out at our full year 2023 results presentation:

- Operating profit: £2bn by 2026.

- Solvency II OFG: £1.8bn by 2026.

- Cash remittances: >£5.8bn cumulative 2024-26.

- Following the completion of the proposed acquisition of Direct Line we expect to reframe the Group targets to reflect the expanded Group.

- In General Insurance we remain focused on pricing appropriately to maintain the strong rate adequacy of the book. We expect a continued improvement in the COR in 2025, subject to normal weather conditions.

- In our Health business we anticipate further growth towards our 2026 ambition of £100m operating profit. In Protection, growth from AIG will moderate, with profits from the acquisition emerging over time as the CSM is released.

- In Wealth we expect our strong growth momentum to continue towards our ambition for £280m operating profit by 2027.

- In BPA we expect to remain active, and we anticipate volumes to remain at similar levels to those achieved over the last three years, although given the exceptional market conditions in 2024 those volumes are not expected to repeat, with our primary focus remaining on margins and IRRs.

Footnotes

- Sales for Insurance (Protection and Health) refers to Annual Premium Equivalent (APE). Sales for Retirement (Annuities and Equity Release) refers to Present Value of New Business Premiums (PVNBP). Premiums for General insurance refer to gross written premiums (GWP). The first instance of each reference has been footnoted. However, this footnote applies to all such references in this announcement. PVNBP, APE and GWP are Alternative Performance Measures (APMs) and further information can be found in the 'Other information' section of the Aviva plc Annual Report and Accounts 2024.

- All GWP movements are quoted in constant currency unless otherwise stated.

- All net flows as a percentage of opening assets under management are annualised.

- Solvency II shareholder cover ratio is the estimated Solvency II shareholder cover ratio at 31 March 2025.

- The shareholders’ resolutions approving the cancellation of the Aviva plc and General Accident plc preference shares were passed on 15th April 2025, with the implementation of the cancellation for: (i) Aviva plc, effective 14 May 2025; and settlement expected on 22 May 2025 and (ii) GA plc, remaining subject to a court order confirming the cancellation and the registration of the court order with the Registrar of Companies. Settlement for GA plc is expected on 12 June 2025. To date, the Solvency II debt leverage ratio pro forma has been adjusted to reflect the £450 million nominal amount of the preference shares.

- 56% of operating profit from capital-light business as at 31 December 2024. Reference to operating profit represents Group adjusted operating profit which is a non-GAAP APM and is not bound by the requirements of IFRS. Further details of this measure are included in the 'Other information' section of the Aviva plc Annual Report and Accounts 2024.

- Rounding differences apply.

Media Contact:

Hazel Tan

Email: hazel.tan@aviva.com

Tel: 437-215-5770

About Aviva Canada

Aviva Canada is one of the leading property and casualty insurance groups in the country, providing home, automobile, lifestyle, and business insurance to 2.5 million customers coast to coast. A subsidiary of UK-based Aviva plc, we have the financial strength, scale and are a trusted insurance provider globally for more than 325 years.

For more information, visit aviva.ca or Aviva Canada’s blog, LinkedIn, and Instagram pages.