Did you know that if your business incurs property damage caused by another party, Aviva will work on your behalf to recover not only the insured losses but also any uninsured losses? Such losses may include expenses you incur to maintain operations or minimize business interruption and even a portion of the deductible.

The process is called subrogation, and we cover the cost so our clients don’t have to worry about additional expenses on their claim.

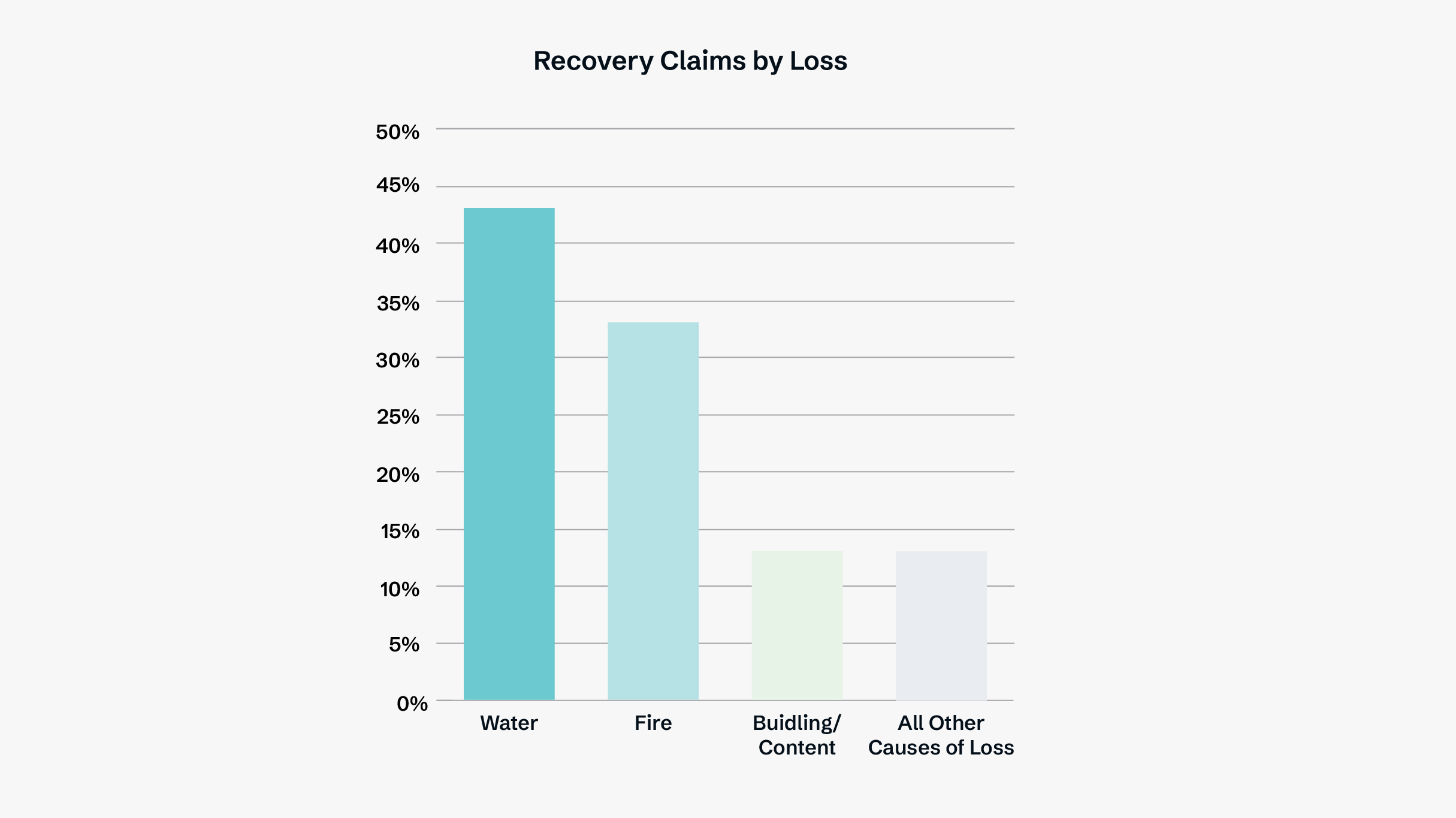

Subrogation opportunities can exist on all types of losses, but our most frequent recovery actions are on water damage. Almost 40% of water damage claims involve a variation of failed plumbing, such as a valve failure or inadequate soldering on a pipe that led to a rupture.

Set your business up for subrogation success

There are actions your business can take to ensure you’re in a good position in the case of a loss that could be eligible for subrogation. The more information and documentation available, the more successful the subrogation is likely to be.

Be prepared for a loss

Detailed records related to your property will help subrogation specialists if there is the potential for recovery. These include:

- up-to-date floor plans, pictures/videos of your property

- precise records of invoices for equipment and warranties, stock, maintenance records

- current inventory lists

- pictures or videos (ideally with date stamps) of what is being insured, i.e. commercial equipment, site plans, leases

- regular maintenance records for your machinery, equipment, supplies, etc

- contracts, work orders, and invoices associated with maintenance and repair contractors

- daily, weekly, and monthly business documentation, such as rental agreements, mortgage information, costs of operation, payroll, sales (helpful for business interruption claims)

- security camera footage, ideally located off-site.

What to do after a loss

It’s important to preserve the scene as much as possible after an incident to demonstrate the scope of the damage and the source of the issue. Good evidence goes a long way in achieving a successful recovery. In a water loss, this might look like preserving the broken valve or broken pipe.

You’ll also want to calculate all uninsured expenses and keep supporting documentation to submit during the claims process. This will ensure our team has what it needs to begin an investigation in a loss that’s eligible for subrogation.

Understand the subrogation process

The subrogation process could be a long one depending on the number of parties involved in the litigation and the number of experts required to substantiate the loss. On average, a subrogation action takes about four years to reach conclusion (sometimes shorter and sometimes longer) and involves multiple steps:

1. Investigate to ascertain the potential at-fault parties.

2. Obtain an expert to comment on the relevant standard of care.

3. Issue a Statement of Claim against the at-fault parties (defendants) detailing why we see they have breached the standard of care.

4. Exchange relevant documents.

5. Attend examinations for discovery—parties ask questions of each other to find out what happened and get their version of events.

6. Eventually, settlement—only rare cases go to trial.

Our subrogation lawyers walk our clients through the entire process and help ensure they are fully prepared.

Ask our subrogation team

If you have questions about subrogation, we invite you to reach out to the leader of our subrogation team: carrie.miller1@aviva.com