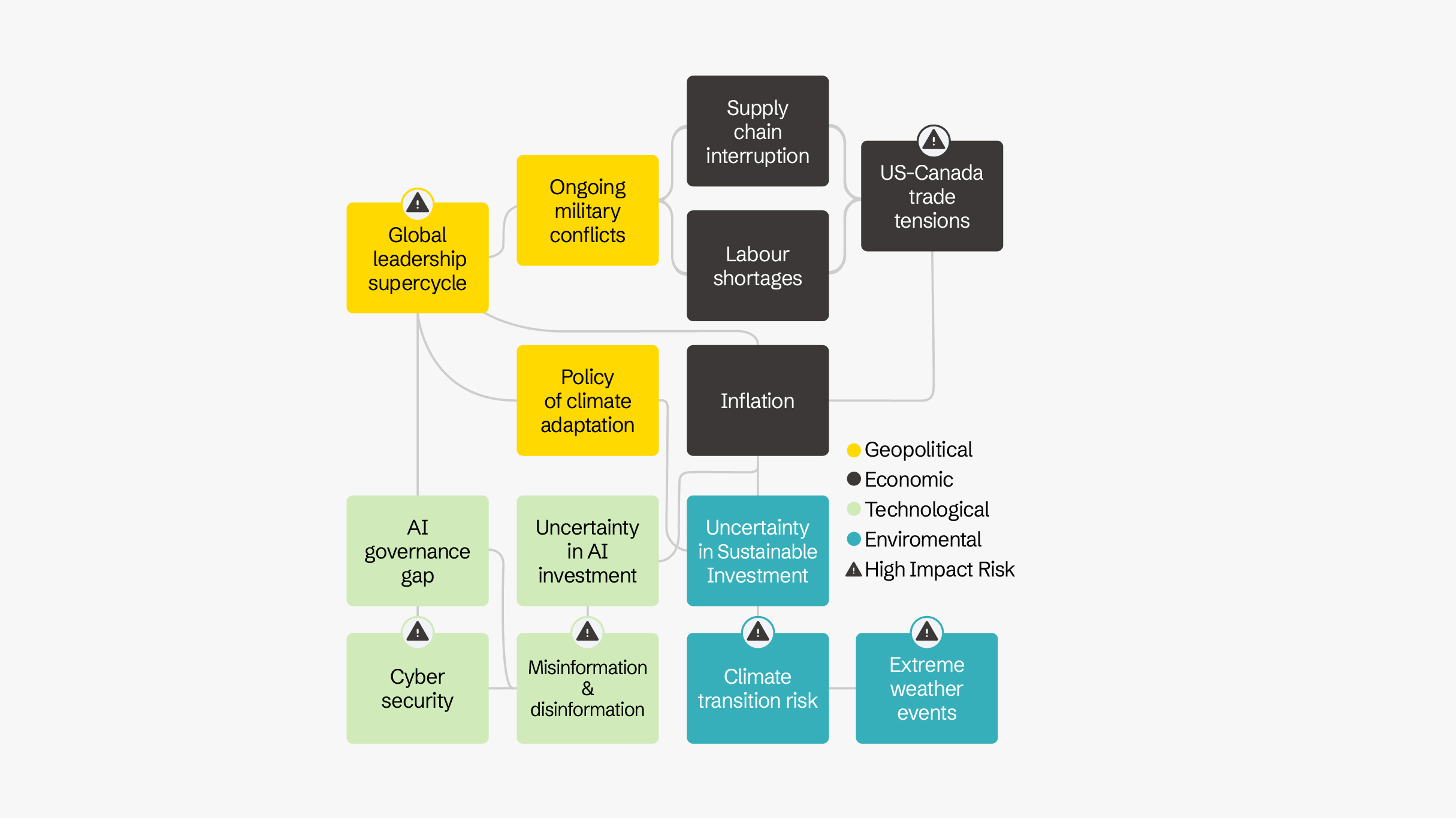

Geopolitical uncertainty, including ongoing conflicts, trade sanctions, and tariff escalations are disrupting supply chains and creating heightened volatility and risk for businesses. Labour shortages, inflation, cybersecurity concerns, and the increasing severity of extreme weather events are compounding these issues.

The world in transition

As the end of the Q4 approaches, business continuity planning should include exploring strategies for mitigating supply chain risks and being realistic about business interruption (BI) exposure. Here are some key considerations.

Ensuring adequate BI coverage

BI coverage is a reactive type of insurance designed to help a business recover financially after a physical damage loss, such as a fire or flood. However, for businesses with a critical dependence on suppliers, complex global supply chains are dramatically increasing BI exposure. The time frames to receive raw materials and complete repairs are lengthening, and the associated dollar losses are going up exponentially.

A critical challenge in modern BI claims is that many companies do not have sufficient monetary limits or indemnity periods. They also may not be aware of coverage add-ons that could help with supply chain challenges and restore the business to pre-loss income levels.

- Indemnity period: The typical indemnity period chosen by businesses in many Canadian BI coverages is 12 months. However, with code upgrades required for older buildings, delays in construction, and global supply chain bottlenecks, rebuilding a facility often takes more than a year.

- Action: Consider extending the BI indemnity period to 18, 24, or 36 months to ensure adequate coverage in the event of a loss.

- Contingent BI coverage: A loss at a key supplier’s or customer’s location can severely impact your revenue. Contingent BI coverage protects you in these scenarios, yet is rarely taken up by companies, leaving a significant gap in resilience.

- Action: Ensure your policy has contingent BI coverage so you’ll get paid if a supplier or customer can’t deliver what you need to do business.

- Expediting and extra expense coverages: Businesses should also ensure they have appropriate limits for crucial add-ons like expediting expense coverage, which can pay to fly in a critical part from overseas rather than wait for shipping. Extra expense coverage can fund additional costs, like advertising, to get your business back to normal operations—and profitability—quicker after reopening.

- Action: Explore expediting and extra expenses add-on coverages.

It’s important to have active conversations with your insurers and brokers to ensure your business has the right level of indemnity and takes advantage of extensions of coverage for specified and unspecified suppliers.

Take a strategic approach to supply chain resilience

As businesses around the world adapt to tariff challenges, there are many strategies in play to mitigate risk. Among them:

- Diversifying supply chain: Working with multiple suppliers across several regions can help reduce the impact of tariffs. Many companies have focused on distributing procurement to vendors exclusively in Canada when possible to avoid US-imposed tariffs. Others seek suppliers in new global marketplaces.

- Exploring Just-in-Time (JIT) and ‘Just-in-Case’ inventory models: Each has a distinct risk profile.

- Just-in-time: This lean model, common in industries like auto manufacturing, minimizes the inventory stored on-site. If a fire occurs, the property exposure is reduced, and it may be easier to rent another facility and get back into business quickly, which lessens the impact on business interruption. However, this strategy creates a critical dependence on third-party suppliers, making Contingent BI coverage essential.

- Just-in-Case: Holding excess inventories—raw materials or finished goods—mitigates the risk of delays from tariffs or supply shocks, allowing a company to fulfill commitments. However, this strategy increases the property exposure if the warehouse is full, and a major loss would severely affect BI and the ability to restart operations.

- Scenario and stress testing: Use risk modeling to test worst-case scenarios, such as port closures, cyber events, or war in key shipping routes. Leveraging AI can provide real-time visibility for early detection of geopolitical or natural catastrophe issues. This type of detailed planning, including written agreements for backup resources, is critical for supply chain resilience.

- Alternative risk financing: Captive risk financing allows a company to form its own licensed insurance subsidiary to finance the more predictable, frequent, lower-severity portion of its risk. This strategic tool offers benefits like customized coverage to fill gaps (e.g., environmental liability) and stabilized pricing that reflects the company’s actual loss experience. Aviva has options.

How Aviva is securing our supply chain

Just like many of our commercial clients, we identified supply chain risks and are working on vertical integration so we have more in-house capabilities. For example, we have internalized a forensic accounting function that helps us quantify damages, settle claims, and work closely with adjusters and examiners to get claims settled.

To reduce our supply chain complexity and tariff concerns, we have purchased vendors such as auto body shops, construction companies, and we’re looking at healthcare businesses so that we can directly serve our clients rather than wait on third party suppliers.

Aviva Risk Management Solutions provides supply chain risk assessments

Aviva Risk Management Solutions (ARMS) helps clients assess and mitigate their supply chain and business interruption risks. ARMS specialists conduct thorough risk assessments that directly impact the understanding of a company’s resilience.

As part of a comprehensive supply chain analysis, we examine the source of raw materials, shipping methods, and dependency on critical equipment to identify exposures and contingency plans for each product. We also help clients develop contingency plans for the loss of a critical supplier or a fire at a facility.

Following the risk assessment, we share a risk report and provide actionable risk improvement recommendations. The output is a detailed understanding of the necessary steps to improve controls and awareness.

For information, reach out to an ARMS specialist at arms.canada@aviva.com.

Update your BI coverage

We encourage you to speak with your broker and an Aviva GCS (Global Corporate & Specialty) underwriter to discuss how we can help you ensure your business has the most comprehensive BI coverage available. This includes the most appropriate loss limits, the most suitable extensions for specified and unspecified suppliers and customers, and, most importantly, an adequate indemnity period that recognizes the key dependencies and supply chain realities for your business.