As 2026 progresses, you might be hearing whispers of a “soft market” in the insurance world. If you look into the reinsurance machinery that underpins our industry, the story is more complex—and it directly impacts your business.

For risk managers and financial decision-makers, understanding the reinsurance market is not just about pricing; it’s about knowing that your insurer has the capital and capacity to stand behind you if a major weather or other event strikes. We’re proud to report that Aviva Canada stands behind our customers with both.

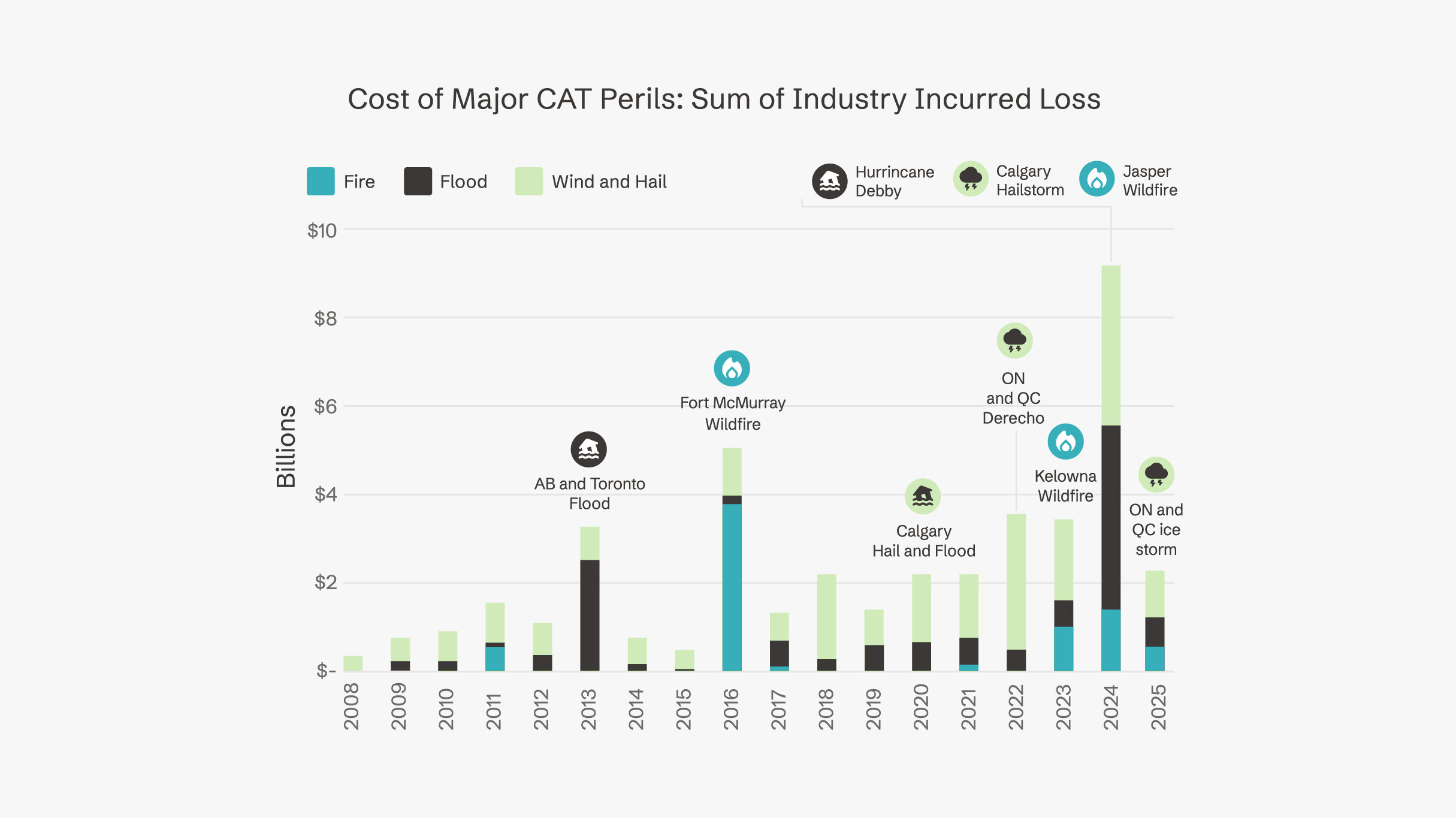

While 2025 offered a welcome reprieve from the relentless natural catastrophes of 2024, the insurance market is still finding its footing in 2026. Reinsurers are remaining cautious, underwriting discipline is tighter, and the “payback” for a volatile decade is still being calculated.

Here is what you need to know about the property, casualty, and surety reinsurance markets for the year ahead.

Property: The long road to recovery

To understand the 2026 property market, it’s helpful to look in the rearview mirror. While Mother Nature was relatively kind to Canada in 2025, the shadow of 2024 looms large. That year could be an anomaly of high-frequency, high-severity events that shattered records and left reinsurers feeling they still haven’t fully recovered.

Even a quiet year like 2025 has not triggered a freefall in reinsurance rates. Reinsurers are wary of being hit every couple of years by massive losses, so they are holding the line on pricing and capacity. For insurers like Aviva, this has meant absorbing losses directly rather than passing them on. We have seen a shift where high-frequency events, like wildfires and floods, are becoming as damaging as the low frequency catastrophes of the past.

The trend line is clear: climate change is driving an increase in both the severity and frequency of these events. For your business, this means the days of relying solely on risk transfer are over. The most sophisticated risk managers are anticipating these trends by protecting their properties against flood and fire before the loss occurs.

Casualty: The disconnect between growth and caution

In the casualty market reinsurers are tightening their belts, driven by fears of inflation and the nuclear verdicts exploding south of the border.

In the US, court awards exceeding $10 million are becoming alarmingly common, driven by aggressive litigation funding and social inflation—a trend where juries are increasingly predisposed to punish large corporations. While Canada has historically been sheltered from these extremes, the psychological and economic spillover is real. Reinsurers view North America as a connected ecosystem; if litigation costs skyrocket in the U.S., the pressure inevitably flows north, impacting pricing for Canadian companies with cross-border exposure.

This divergence creates a unique dynamic for 2026. There may be softer pricing on primary policies where there is little to no claims activity. However, while the casualty market remains competitive, the knowledge of US losses and exposure has influenced Canadian underwriters to reflect on and ensure adequate pricing and limits for US exposures and risks. On umbrella and excess layers, where there are tough classes and reinsurers are heavily involved, there will be some price stabilization or even increases. But insurers will be competing for loss-free businesses.

Consider retention amounts—what your company can afford to retain on any potential claim. This can reduce the upfront payout, but it may cost you more if a claim does occur.

We’re also seeing significant contraction in facultative reinsurance. Unlike “treaty” reinsurance, which covers an insurer’s entire portfolio of policies, facultative reinsurance is negotiated for a specific, individual risk. It is typically used for high-value or complex accounts that don’t fit neatly into standard agreements.

Capacity in this specific market has declined notably in Canada over the last few years. Reinsurers are withdrawing from the space due to slowly deteriorating results and a lack of new market entrants. Even when capacity is available, the terms offered are often at odds with the primary market, making them commercially unviable. Coverage for difficult exposures—such as opioids or PFAS (forever chemicals)—is rarely considered on a facultative basis anymore. This contraction means that for large, complex risks, insurers have fewer levers to pull, placing even more emphasis on your individual risk management practices.

Looking ahead

As we head deeper into 2026, the key for your business is to look beyond the premium line item. By investing in robust risk management—whether that means climate-proofing your facilities or tightening quality controls to prevent liability claims—you position your company not just as a customer, but as a preferred partner to the reinsurance market.

For more information, speak with your insurance broker or contact us at gcs.ca@aviva.com