The narrative of Canada’s commercial insurance sector shifted significantly in 2025. After a prolonged hard market characterized by tight capacity and rising costs, we transitioned into a more competitive environment, with rate decreases appearing across several major lines.

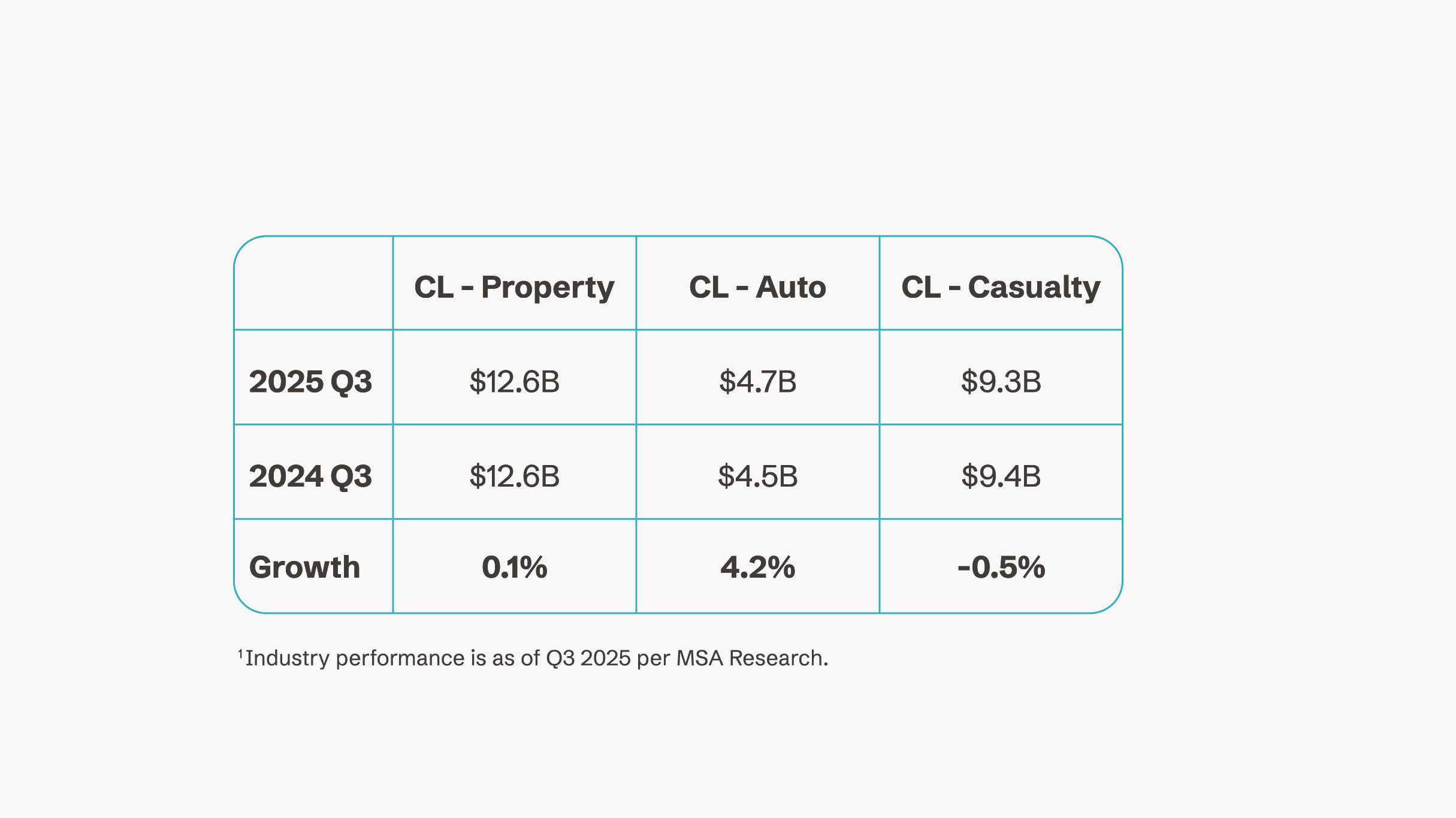

This change has been driven by a number of factors: improved underwriting results, higher investment income, and increased market capacity. For decision-makers, the data tells a clear story. According to Q3 2025 industry performance metrics, the liability segment shrank by -0.5%, while property remained relatively flat with just 0.1% growth. Those negative premium changes, factoring in economic growth and inflation, showed some sizable rate decreases.

Q3 2025 Industry growth by line of business.

While new entrants and incumbent insurers are expanding their risk appetites, the market remains nuanced. Property coverage is still costly in catastrophe-prone regions, and challenges like climate-driven losses, social inflation, and economic uncertainty persist.

The volatility trap

For risk managers, a softening market is generally welcome news. However, history tells us that market cycles can be deceptive. While the current environment favours the insurance buyer, what customers and insurers alike truly require is stability.

Extreme swings—from sharp price hikes to plummeting premiums—create unpredictability that makes long-term business planning difficult. We are currently seeing an influx of supply, particularly from overseas markets like London, which is driving aggressive pricing. While it is tempting to chase the lowest possible rate in the short term, what goes down must come up.

The most dangerous outcome for a risk manager is to partner with an insurer that buys business during a soft market only to retrench or exit the line entirely when claims activity rises or investment returns dip. We have seen this cycle play out for decades.

Quote broadly, stay disciplined

In this environment, our philosophy is straightforward: we remain open to all business within our risk appetite, but we refuse to chase pricing that is disconnected from sound risk fundamentals. This approach is not about inflexibility; it is about preservation. We are prioritizing stability over short-term wins to prevent future rate spikes and volatility for our clients.

There is a distinct difference between a soft market and an unsustainable one. If pricing drops below the threshold required to cover future claims—particularly in a world where catastrophic weather event frequency is increasing —the market is setting itself up for a dramatic correction. By maintaining our pricing discipline, we can offer a consistent, predictable partnership through 2030 and beyond.

The hidden cost of switching

Beyond the premium line item, there is a tangible cost to volatility. Chasing the lowest rate often requires switching carriers, which could introduce friction into your organization.

It’s critical to consider the strength of the claims service and capabilities with legacy insurers. You want to know you’ve got an expert team with a proven process to get you back in business quickly after a claim. Changing insurers also disrupts established relationships with these claims teams and risk engineers. It could also create administrative burden to your internal teams as they adapt to new processes, new reporting requirements, and new points of contact. A long-term relationship with a reliable partner allows you to flow with the market— benefiting from softening rates—while cutting off the extremes at the upper and lower ends.

The case for a solid domestic partner

In a business environment that increasingly values local resilience and continuity, the strategic advantage of working with a Canadian-domiciled insurer has never been clearer.

- Local expertise: No one understands Canadian risk like a Canadian insurer. Aviva has proprietary data on local regulations, geography, and severe weather patterns. This allows for more precise underwriting and faster, context-appropriate responses to events like wildfires and floods.

- Customized solutions: We design products specifically for the Canadian market, ensuring policy wordings are fully compliant with local legal frameworks.

- Global innovation, locally applied: As part of a global network, we leverage expertise from Aviva UK to expand complex coverages in areas like renewable energy and cyber. We then adapt these solutions for the Canadian reality rather than offering plug and play answers.

- Deep relationships: In a complex geopolitical climate, businesses are prioritizing deeper relationships with their vendors. We aim to be a single strategic partner, offering support across multiple lines of business to build the trust necessary for long-term stability.

A wiser investment

Ultimately, the decision to prioritize a domestic insurance partner is a practical one. It maximizes efficiency, minimizes complexity, and ensures an expert response when it matters most.

As we move through 2026, rates may stabilize, and the market may fluctuate. But our commitment remains the same as it has been for hundreds of years: to be the stable, resilient partner your business needs to navigate whatever comes next.

For more information, speak with your insurance broker or contact us at gcs.ca@aviva.com